2026-05-21

SBA 7(a) Loans for Assisted Living Facilities: A Funding Guide

By Kevin Bartley

America is aging fast, and the assisted living industry is racing to keep up. The 80-plus population is growing nearly 5% annually through 2030, while new facility supply is barely keeping pace at 1–2% per year. That gap is creating one of the most durable demand curves in any small business category today.

The numbers tell the story. The U.S. assisted living facility market hit $45.5 billion in revenue in 2024 and is forecast to reach $93.54 billion by 2033. Roughly 15,937 facilities operate across the country right now, and that figure isn't enough — the 85-plus population alone is projected to more than double, from 6.6 million in 2019 to 14.4 million by 2040.

But here's the catch. Assisted living facilities are capital-intensive operations. Real estate, equipment, licensing, staffing, working capital — the upfront costs lock out most operators before they even open the door. Traditional banks tend to balk at the hybrid commercial-residential nature of these properties, and conventional financing rarely covers both the business and the building in a single loan.

That's why the SBA 7(a) loan has become the go-to financing tool for assisted living operators. In the following blog, we'll show you how SBA 7(a) loans work for assisted living facilities, what they fund, and how to qualify.

The Assisted Living Capital Crunch: Why Conventional Financing Falls Short

Senior care is a high-leverage business with high-leverage costs. Average revenue per assisted living facility location is approximately $2.3 million, but profit margins are modest at 6.9%, with wages taking up 42.7% of revenue. That math leaves little room for big down payments or short-term debt.

Conventional lenders also struggle with the assisted living asset class itself. The properties are legally residential but operate as licensed commercial businesses. Most banks don't know how to underwrite that hybrid — and when they do, they typically demand 25–35% down, shorter terms, and full collateralization.

For an operator looking to acquire a $3 million facility, that's a wall.

So what's the alternative? Yes, the answer is the SBA 7(a) loan. It was built for exactly this kind of capital-heavy small business, and it solves the financing problem that has historically kept good operators on the sidelines.

Here's why.

SBA 7(a) Loans for Assisted Living Facilities: A Game-Changer for Senior Care Operators

The SBA 7(a) loan is the Small Business Administration's flagship financing program. It provides up to $5 million in government-guaranteed capital — and through companion loan structures, total project financing can reach $6.5 million or more. For assisted living operators, that's the difference between a long pipeline of acquisition targets and an empty deal sheet.

What makes SBA 7(a) loans for assisted living facilities different from conventional debt:

- Long amortization — up to 25 years for real estate, up to 10 years for working capital and goodwill, which keeps monthly payments manageable

- Lower equity requirements — typically 10% down on acquisitions, compared to 25–35% for conventional commercial loans

- Single-loan financing — covers business goodwill, real estate, equipment, and working capital in one transaction, not three separate facilities

The 7(a) program also finances both established acquisitions and ground-up construction. So whether you're buying a 30-bed facility from a retiring owner or breaking ground on a new memory care community, the structure adapts.

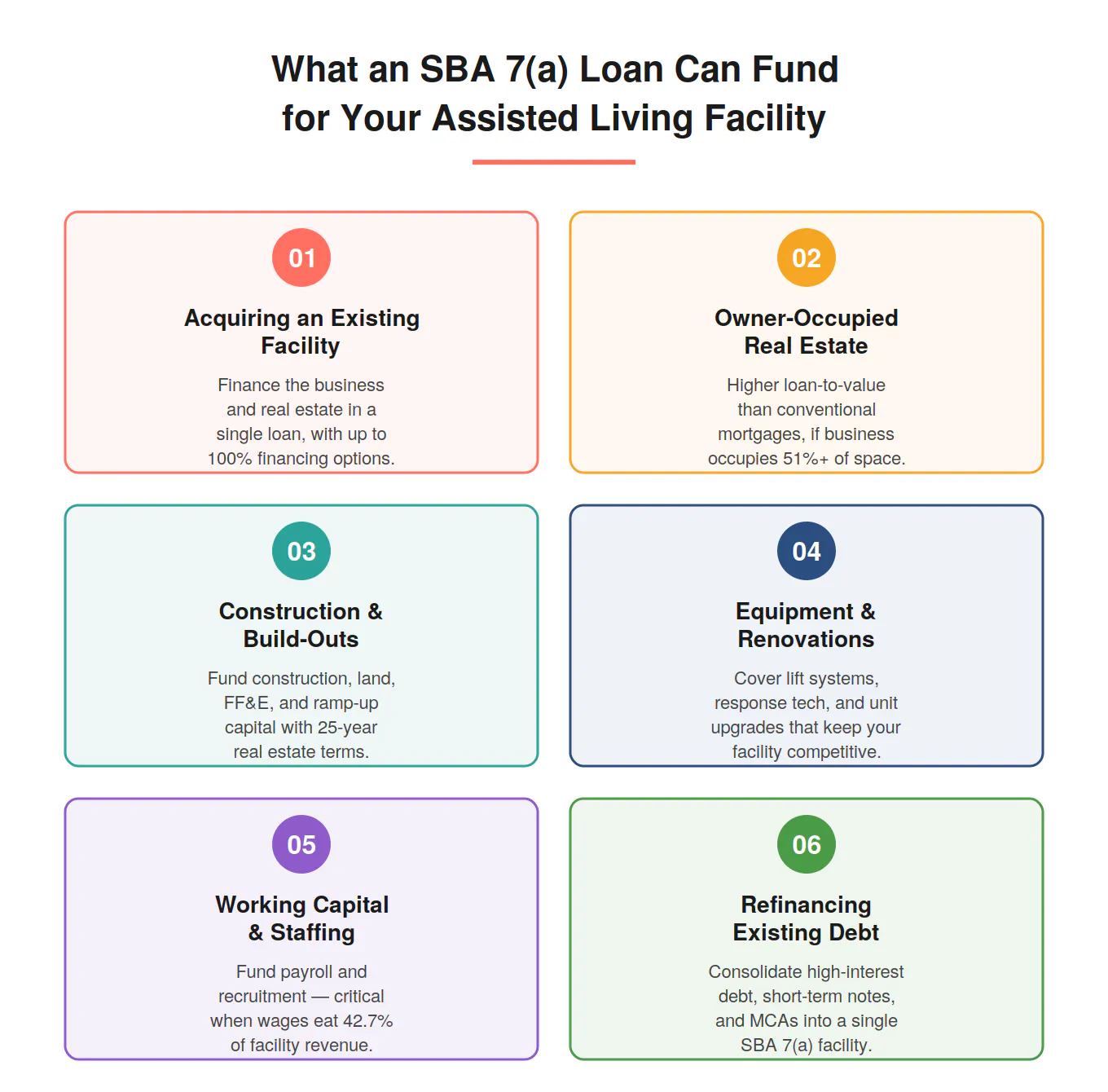

What an SBA 7(a) Loan Can Fund for Your Assisted Living Facility

The SBA 7(a) is one of the most flexible loan products available to senior care operators. The program covers nearly every capital need a facility owner faces — from day-one acquisition to long-term expansion. For a broader view of how operators deploy 7(a) capital, see Port 51's breakdown of the top 10 ways companies use SBA 7(a) loans.

Here's a closer look at the most common use cases for assisted living facilities.

Acquiring an Existing Facility

Buying an established assisted living business is the most common SBA 7(a) use case in the senior care space. The program finances both the operating business and the real estate in a single loan — something conventional lenders rarely do. Experienced operators with at least one profitable facility already under management may even qualify for 100% financing with no down payment.

For first-time buyers, the standard structure requires roughly 10% equity, which can come from cash, seller financing on full standby, or outside investors holding less than 20% of the new entity. To go deeper on this, Port 51's guide to funding a business acquisition with an SBA 7(a) loan walks through the structure in detail.

Owner-Occupied Real Estate Purchase

If your facility owns its own building, SBA 7(a) financing covers the real estate at a higher loan-to-value ratio than most conventional commercial mortgages. The main requirement: your business must occupy at least 51% of the property. For assisted living facilities, that threshold is almost always cleared by default.

Ground-Up Construction and Build-Outs

Building a new facility — or expanding an existing one — is a major capital event. SBA 7(a) loans finance new construction, land acquisition, soft costs, FF&E, and the initial working capital reserves needed to ramp up to stabilized occupancy. The 25-year amortization on real estate makes monthly debt service workable even during the lease-up period.

Equipment, Renovations, and Refurbishments

From lift systems and emergency response equipment to full unit renovations, SBA 7(a) loans cover the capital expenditures that keep a facility competitive. Modern residents — and their adult children making the placement decision — expect amenities, technology, and updated finishes. The 7(a) funds that upgrade cycle without forcing you to choose between cash flow and capex.

Working Capital and Staffing

With wages consuming 42.7% of revenue, payroll is the single largest cost for any assisted living operator. SBA 7(a) loans can fund working capital reserves to cover staffing during slow occupancy periods, recruitment for high-turnover roles, and the everyday operating costs that keep care levels consistent.

Refinancing Existing Debt

Many operators are sitting on legacy debt — high-interest commercial mortgages, short-term notes, or merchant cash advances — that's strangling cash flow. The SBA 7(a) refinance extends term, lowers monthly payments, and consolidates multiple obligations into a single facility. The catch: the refinance must improve cash flow and meet the SBA's benefit tests.

Qualifying for an SBA 7(a) Loan for an Assisted Living Facility

The SBA 7(a) program is flexible, but it isn't a blank check. Lenders evaluate every applicant against a consistent set of criteria. For a full breakdown, see Port 51's SBA loan requirements page.

Here's what underwriters look at for assisted living facility loans:

- Credit and character. Most lenders look for a personal credit score of 680 or higher, though stronger cash flow can offset weaker credit. All owners with 20% or more equity must provide a personal guarantee.

- Industry experience. Senior care is a regulated, operationally complex industry. Lenders strongly prefer applicants with direct operational experience — whether as an owner, administrator, director of nursing, or similar role. First-time operators can still qualify, but the business plan and management team carry more weight.

- Equity injection. Acquisitions typically require 10% equity at minimum. Construction loans often require slightly more. Equity can come from cash, retirement rollovers (ROBS), seller financing on standby, or qualified outside investors.

- Cash flow. This is the single most important factor. The facility — or the target being acquired — needs to demonstrate enough cash flow to cover debt service with a healthy cushion, typically a debt service coverage ratio of 1.25x or better.

- Licensing and compliance. State licensure, life safety code compliance, and any required certifications must be in order. Lenders will want to see the current license, recent inspection reports and any outstanding deficiencies.

- Business plan and projections. A start-up or expansion requires a detailed business plan with realistic projections on occupancy and revenues. Lenders want to see assumptions backed up with market data, not optimism.

The Speed Advantage: Why Non-Bank SBA Lenders Matter for Assisted Living Deals

Senior care deals move fast. Sellers want certainty, sellers want speed, and a slow lender can kill a deal at any stage. Traditional banks often take 90 days or longer to close an SBA 7(a) loan — and that's when nothing goes wrong.

That's why non-bank SBA lenders have reshaped the market. Lenders with Preferred Lender Program (PLP) status can underwrite, approve, and close SBA-guaranteed loans in-house, cutting weeks off the timeline. Port 51 Lending, for example, closes SBA 7(a) loans in an average of 27 days — roughly a third of the time most banks take.

For assisted living acquisitions, that speed matters. A 30-day close lets you compete with cash buyers, lock in seller terms, and take over operations before census drift or staff turnover erodes the business.

Port 51's deep-dive on SBA 7(a) loans and faster financing with non-bank lenders goes into more detail on why specialization matters.

The Results: What SBA 7(a) Financing Delivers for Assisted Living Operators

When structured correctly, an SBA 7(a) loan transforms what's possible for a senior care operator. Here's what well-structured 7(a) financing typically delivers:

- Up to 90% leverage on acquisitions, freeing capital for working capital reserves, renovations, and ramp-up staffing

- 25-year amortization on real estate components, lowering monthly debt service by 30–40% compared to conventional 10–15 year commercial mortgages

- Single-loan execution that consolidates real estate, goodwill, equipment, and working capital — eliminating the friction of stacking multiple financing sources

For experienced operators, the impact compounds. A second or third facility acquired with little or no down payment becomes a portfolio play, not a one-off purchase.

Build Your Assisted Living Facility with the Right SBA Lender

The senior care opportunity is real, the demand curve is durable, and the financing tool is sitting right there. SBA 7(a) loans for assisted living facilities solve the capital problem that has historically kept good operators out of the market — covering real estate, goodwill, working capital, and expansion in a single, long-amortization loan.

Port 51 Lending specializes in structuring SBA 7(a) loans for industries like assisted living, where speed, cash flow analysis, and operator experience matter more than rigid lending formulas. With an average close time of 27 days and companion loans of up to $6.5 million, Port 51 helps senior care operators move fast on the deals that build durable businesses.